I. Event Recap: From Legacy Hardware Vendor to AI Infrastructure Powerhouse

On July 9, 2026, Hewlett Packard Enterprise (HPE) released its fiscal Q2 2026 earnings, delivering a bombshell to the tech industry. Revenue reached $10.68 billion, surging 40% year-over-year—a growth rate that not only smashed Wall Street expectations but also marked HPE's official transition from a traditional server and storage vendor to a core player in AI infrastructure.

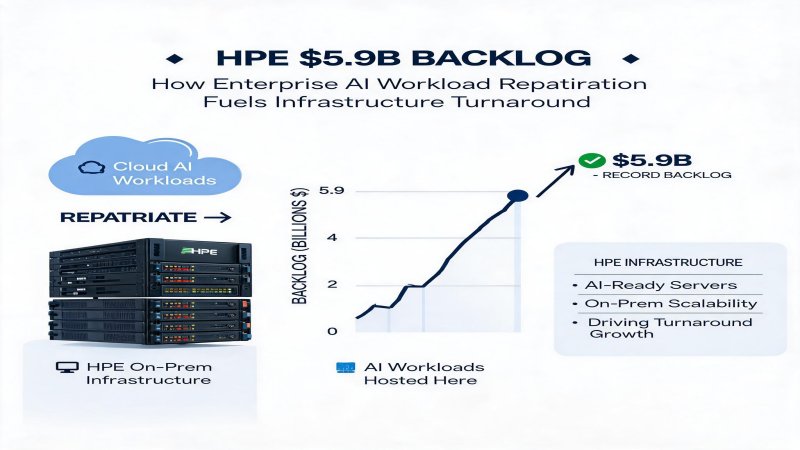

Even more striking, HPE's backlog hit a record $5.9 billion at quarter-end. Backlog represents orders placed but not yet delivered, directly reflecting demand that far outstrips current supply capacity. On the earnings call, management candidly admitted that demand for AI systems and traditional servers is "growing faster than we can ship them."

HPE's AI transformation did not happen overnight. The 2025 acquisition of Juniper Networks was the critical inflection point, giving HPE the ability to offer an integrated compute-networking-storage stack for the first time. In Q2 FY2026, traditional server orders tripled—indicating that growth is being driven not only by high-end AI servers but also by enterprises building inference and agentic AI capabilities on-premise.

Financially, networking revenue reached $2.7 billion with 21.6% operating margins, contributing over 40% of total operating income. Management raised full-year earnings guidance by over 40%, and the stock has risen 81% year-to-date.

II. Technical Deep Dive: Why the Integrated Stack Matters for Enterprise AI

To understand HPE's rise, one must grasp the technical value proposition. In the generative AI era, the core challenge is not raw compute but orchestrating GPU clusters, high-speed networking, storage, and software into a scalable, low-latency, manageable production environment.

HPE's architecture centers on ProLiant and Apollo servers, Juniper QFX/PTX networking for high-speed interconnect, and Alletra storage for high-throughput data access. In AI training, network latency directly determines GPU utilization—if the network bottlenecks, expensive GPU clusters sit idle. Juniper's RoCE and AI-optimized topologies reduce inter-node latency to microsecond levels.

The Apollo 6500 Gen10 Plus supports up to 8 NVIDIA H200 GPUs with NVLink/NVSwitch interconnect, while Alletra 6000 storage delivers up to 40GB/s throughput. Beyond hardware, HPE's "AI Factory" concept offers certified NVIDIA DGX BasePOD systems, Machine Learning Development Environment (MLDE) software, and GreenLake as-a-Service delivery—allowing subscription-based consumption rather than large upfront CapEx.

III. Financial Logic: Decoding the $5.9 Billion Backlog

The $5.9 billion backlog is a complex signal. It confirms voracious demand but also exposes supply chain constraints limiting revenue conversion.

Server business (Compute) contributes the largest revenue share, but networking (Juniper) at 21.6% operating margins is the primary profit driver—traditional server gross margins typically range 10%-15%, while networking equipment can exceed 40%. As Juniper products pull through larger server and storage deals, overall margins should improve.

However, backlog realization depends on key components, especially NVIDIA GPUs and HBM memory. HPE trades at roughly 13x forward P/E, compared to NVIDIA's 30x+ and Dell's ~15x, suggesting valuation upside remains.

GreenLake's expansion shifts revenue recognition from one-time hardware sales to recurring revenue—compressing near-term cash flow but improving long-term customer lifetime value.

IV. Strategic Landscape: HPE vs Cisco vs Dell vs Arista

| Dimension | HPE | Cisco | Dell | Arista |

|---|---|---|---|---|

| AI Servers | Apollo + ProLiant | Partner-dependent | PowerEdge XE | None |

| Networking | Juniper (acquired) | Nexus/Catalyst dominant | Weak | Market leader |

| Storage | Alletra + GreenLake | HyperFlex limited | PowerStore | None |

| Full Stack | Complete | Network-centric | Compute+storage | Network only |

| As-a-Service | GreenLake mature | Transitioning | APEX small scale | None |

| AI Backlog | $5.9B | $2B+ disclosed | Not disclosed | Not disclosed |

| P/E Ratio | ~13x | ~18x | ~15x | ~35x |

V. Challenges and Risks: Supply Bottlenecks and Cloud Pushback

First, supply constraints. Core components—NVIDIA GPUs and HBM—remain supply-constrained. Management acknowledged demand exceeds shipping capacity, potentially driving customers to competitors.

Second, cloud vendor competition. AWS Outposts, Azure Stack, and Google Anthos extend public cloud capabilities to on-premise data centers. If enterprises prefer "cloud extension" over self-built infrastructure, HPE's addressable market shrinks.

Third, technology路线 risk. HPE's AI servers heavily depend on NVIDIA GPU ecosystem. As AMD MI series, Intel Gaudi, and custom ASICs rise, maintaining multi-platform compatibility increases R&D complexity.

Finally, M&A integration risk. While strategically vital, cultural and product integration with Juniper requires time. History shows large tech acquisitions do not always succeed.

VI. Conclusion and Recommendations

For Enterprise IT Decision Makers: HPE's integrated AI stack and GreenLake as-a-Service model represent one of the most mature on-premise AI deployment solutions available. If your organization plans private AI infrastructure with emphasis on one-stop service and flexible payment, HPE belongs on the shortlist. Order 6-9 months in advance to mitigate supply bottlenecks.

For Investors: At ~13x P/E, HPE remains undervalued within AI infrastructure. The $5.9B backlog provides high revenue visibility for the next 4-6 quarters. Watch Q3-Q4 gross margin trends and Juniper integration progress. If backlog conversion improves and margins expand, 20%-30% upside remains plausible.

For Competitors: HPE's full-stack strategy is redefining competitive rules. Cisco must accelerate server/storage capabilities; Dell must strengthen networking—or risk marginalization.

Forward Predictions:

- Q3-Q4 2026: HPE backlog will grow to $6.5-7B, but supply constraints may persist into early 2027.

- H1 2027: As HBM supply eases, revenue growth should sustain 30%+, with GreenLake recurring revenue exceeding 25%.

- H2 2027: HPE may introduce AMD GPU-based alternatives to reduce NVIDIA dependency.

Why it Matters

Enterprise AI infrastructure is entering its second wave—investment shifting from hyperscaler cloud data centers to on-premise AI capabilities. HPE's $5.9B backlog validates its full-stack plus as-a-service model. As demand for AI inference and agentic AI explodes, enterprises need controllable, secure, low-latency local compute, precisely where HPE's GreenLake offering excels. At 13x P/E, HPE remains undervalued in the AI infrastructure sector.

DECISION

Enterprise IT buyers: Include HPE in shortlist for private AI infrastructure, place orders 6-9 months ahead; prefer GreenLake subscription to reduce CapEx. Investors: 13x P/E offers margin of safety; monitor Q3 gross margins and backlog conversion. Competitors: Cisco must fill server/storage gaps; Dell must strengthen networking.

PREDICT

Q3-Q4 2026: HPE backlog will grow to $6.5-7B, supply constraints persist into early 2027. H1 2027: Revenue growth sustains 30%+ as HBM supply eases; GreenLake recurring revenue exceeds 25%. H2 2027: HPE may introduce AMD GPU alternatives to reduce NVIDIA dependency.

Get 3-5 key AI infrastructure signals weekly →

💬 Comments (0)