I. Event Recap: A Record-Breaking Supercycle

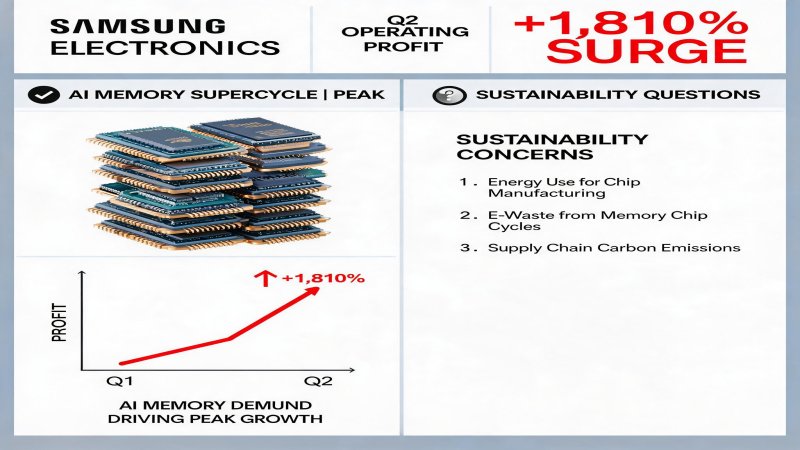

On July 7, 2026, Samsung Electronics released its Q2 2026 earnings guidance, stunning global markets with unprecedented numbers. The company reported operating profit of 89.4 trillion KRW (approximately $66 billion USD), up over 1,810% year-over-year, with revenue reaching 171 trillion KRW (approximately $127 billion USD), up approximately 129% YoY. This single-quarter profit not only exceeded market consensus by about 6% but also surpassed the historical records of global tech giants including NVIDIA and Apple, and was more than double Samsung's full-year 2025 operating profit of 43.6 trillion KRW.

On a quarter-over-quarter basis, operating profit surged 56% from Q1's 57.2 trillion KRW, with revenue continuing its upward trajectory from already elevated levels. Since Q4 2025, Samsung has set consecutive quarterly records for both operating profit and revenue for three straight quarters. Notably, despite the blowout results, market reaction was mixed: Samsung's Korean shares opened lower and extended losses to nearly 6%, while competitors SanDisk and Micron also declined in after-hours trading.

Timeline recap: Q2 2025 operating profit was merely 4.7 trillion KRW, near trough levels. Beginning Q4 2025, fueled by AI infrastructure buildout, memory chip prices entered a rapid ascent. Q1 2026 profit jumped to 57.2 trillion KRW, and Q2 2026 exploded to 89.4 trillion KRW, completing a nearly 20-fold YoY increase. Samsung will release full Q2 earnings on July 30, disclosing net profit and detailed segment breakdowns.

II. Technical Deep Dive: The HBM-DRAM-NAND Trinity

The primary driver of Samsung's earnings explosion is the Device Solutions (DS) division, particularly memory chips. Under sustained AI infrastructure expansion, data center demand for High Bandwidth Memory (HBM), high-capacity DRAM, and enterprise SSDs remains robust.

HBM is the star of this supercycle. NVIDIA and AMD's flagship AI GPUs all rely on HBM for memory, and HBM supply expansion significantly lags demand growth. Samsung's HBM3E product has achieved mass production at 12-layer stacking, with 36GB per die and bandwidth exceeding 1.2TB/s. In comparison, SK Hynix introduced 16-layer HBM3E with 48GB per die by late 2025; Micron pursues a different packaging approach. For the upcoming HBM4 generation, Samsung plans advanced hybrid bonding technology to exceed 16 layers, targeting 64GB per die and bandwidth surpassing 2TB/s.

DRAM also shows strong price appreciation. Q2 2026 DRAM ASP rose 44% QoQ, driven by AI server demand for high-capacity DDR5 modules. Samsung leads in 1b-nanometer (approx. 12nm) DRAM process, with 32Gb DDR5 chips in mass production, enabling 128GB server DIMMs.

NAND Flash prices surged 53% in Q2 2026, with enterprise SSD demand as the primary catalyst. Samsung's 9th-generation V-NAND exceeds 290 layers, with approximately 50% higher bit density than its predecessor, and remains at the forefront of QLC technology.

However, Samsung does not dominate alone. SK Hynix currently leads in HBM market share with tighter NVIDIA bundling; Micron is accelerating its 1-gamma DRAM process. Samsung's advantage lies in the most complete memory portfolio (DRAM + NAND + HBM), enabling one-stop procurement for AI data center customers.

III. Financial Logic: From the Brink to the Summit

Samsung Electronics completed a stunning V-shaped recovery. In Q2 2025, operating profit was just 4.7 trillion KRW, with the chip business near breakeven. Just one year later, quarterly operating profit exploded to 89.4 trillion KRW, nearly a 20-fold increase.

From a segment perspective, the DS (Device Solutions) division contributes over 90% of operating profit. In 2025, Samsung's semiconductor operating margin was approximately 15%; by Q2 2026, this metric likely exceeded 35%. The improvement stems from two factors: substantial memory price increases (DRAM +44% QoQ, NAND +53% QoQ), and the rapid revenue mix shift toward high-value HBM products.

Capital expenditure for 2026 is expected at approximately $36 billion, with roughly 70% directed to memory operations, primarily for HBM capacity expansion and advanced DRAM process migration. Despite elevated capex, strong cash flow generation (Q2 2026 operating cash flow estimated to exceed $10 billion) keeps net debt at manageable levels.

From a valuation perspective, despite the earnings explosion, Samsung's forward P/E remains at 12-14x, below SK Hynix's 18x and Micron's 15x. This reflects market concerns about sustainability—investors worry current memory price peaks are cyclical rather than structural.

IV. Strategic Depth: Competitive Matrix

| Dimension | Samsung Electronics | SK Hynix | Micron Technology |

|---|---|---|---|

| HBM Market Share (Q1 2026) | ~35% | ~45% | ~20% |

| HBM3E Stack Layers | 12 (production) / 16 (R&D) | 16 (production) | 12 (production) |

| DRAM Process Node | 1b nm (production) / 1c nm (R&D) | 1b nm (production) | 1β nm (production) / 1γ nm (pilot) |

| NAND Stack Layers | 290 (V9) | 321 (announced) | 232 (production) / 276 (R&D) |

| Key AI Chip Customers | NVIDIA (partial), self-developed | NVIDIA (primary), AMD | NVIDIA (partial) |

| Q2 2026 Operating Profit Growth | +1,810% | ~+300% (est.) | ~+150% (est.) |

| Production Capacity (wafers/month) | Largest | Medium | Smaller |

SK Hynix excels in HBM technology leadership and close NVIDIA partnership. In HBM3E, SK Hynix was first to 16-layer mass production, seizing the high-end HBM high ground. Micron, while smaller in scale, has noteworthy technology reserves in 1γ DRAM and GDDR7.

Strategically, Samsung announced in May 2026 the withdrawal from China's home appliance market to concentrate resources on high-value semiconductors. This decision followed intensifying competition from domestic Chinese brands and Samsung's first annual loss in China since entering the market in 2025.

V. Challenges and Risks: How Long Can the Supercycle Last?

Despite stellar results, Samsung faces significant challenges.

First, markets have preemptively priced in cyclical concerns. Following the earnings surprise, Samsung shares fell rather than rose, with Korean shares dropping up to 6% and KOSPI extending losses to 6%. This reflects investor worries about AI infrastructure ROI—markets fear AI buildout may slow in 2027, dragging memory demand.

Second, HBM technology competition is intensifying. SK Hynix's first-mover advantage in HBM3E may extend to HBM4, while Micron is also increasing HBM investment. If Samsung falls behind SK Hynix in HBM4 mass production timelines, market share could erode further.

Third, geopolitical risks persist. US semiconductor export controls to China may affect operations at Samsung's Xi'an and Suzhou facilities. While Samsung is migrating cutting-edge processes back to Korea, capacity adjustments take time and may increase production costs.

Fourth, Chinese memory vendors pose a long-term threat. YMTC is rapidly advancing in NAND technology, while CXMT is accelerating DRAM catch-up. While currently serving domestic demand, Chinese capacity expansion and technology upgrades could materially impact global memory markets after 2028.

Fifth, "AI bubble" debates may affect capex rhythms. Some Wall Street analysts warn that current AI infrastructure investment may be excessively aggressive. If AI application commercialization underperforms, cloud vendors could cut capex in 2027, triggering a cliff-like drop in memory demand.

VI. Conclusion: Staying Clear-Headed at the Peak

Samsung Electronics' Q2 2026 performance is undeniably historic. With 89.4 trillion KRW in quarterly operating profit and 1,810% YoY growth, Samsung has cemented its dominance in the AI memory supercycle. For investors, Samsung shares remain attractive: forward P/E below key competitors, scale advantages that are difficult to challenge, and a diversified memory portfolio providing multiple revenue growth avenues.

For data center procurement decision-makers, the following strategies are recommended:

- Short-term (6-12 months): Memory prices remain in an upward channel. Consider locking in long-term contract prices ahead of potential further increases in Q4 2026 to Q1 2027.

- Medium-term (1-2 years): Closely monitor HBM4 technology progress and mass production timelines. If Samsung regains technology leadership in HBM4, pricing power will strengthen further; otherwise, SK Hynix may continue expanding HBM share.

- Long-term (3-5 years): Evaluate Chinese memory vendors' technology progress and capacity expansion impacts on global pricing. Maintain supplier diversification to avoid over-dependence on a single vendor.

Predictions:

- Q3 2026: Samsung operating profit likely holds at 80-90 trillion KRW, but QoQ growth will slow markedly, signaling the supercycle entering a plateau phase.

- H1 2027: HBM4 begins small-volume shipment. Samsung-SK Hynix competition in high-end HBM will intensify, with technology route selection (hybrid bonding vs. thermocompression bonding) becoming a critical differentiator.

- H2 2027: If AI application commercialization proceeds smoothly, memory demand remains robust. If AI investment corrects, DRAM and NAND prices may retreat 20-30% from peaks, while HBM prices should remain relatively stable.

- 2028: Chinese memory vendors may reach global tier-2 levels in NAND and achieve technology self-sufficiency in DRAM, potentially evolving the global memory market from a "three-horse race" to a "four-way competition."

Why it Matters

Samsung's single-quarter profit has surpassed the historical records of NVIDIA and Apple, signaling a shift in global semiconductor profit centers from logic to memory chips. AI infrastructure buildout is entering its most aggressive expansion phase, with global semiconductor market size projected at $1.51 trillion in 2026. Samsung's production scale advantage makes it the biggest beneficiary of the supercycle, but SK Hynix's HBM technology lead and US-China tech decoupling risks are key variables.

DECISION

Investors: Samsung's forward P/E of 12-14x is below SK Hynix and Micron, offering valuation safety margins, but monitor whether Q3 profit growth decelerates.

Data center procurement managers: Consider locking in long-term memory contracts 6-12 months ahead to avoid further price increases in Q4 2026-Q1 2027.

Supply chain decision-makers: Maintain dual-sourcing strategy for HBM between Samsung and SK Hynix to reduce single-supplier risk.

PREDICT

Q3 2026: Samsung operating profit likely holds at 80-90 trillion KRW, but QoQ growth will decelerate markedly.

H1 2027: HBM4 begins small-volume shipment; Samsung vs. SK Hynix technology route competition (hybrid bonding vs. thermocompression bonding) becomes critical.

H2 2027: If AI application commercialization proceeds smoothly, memory demand remains robust; if investment corrects, DRAM and NAND prices may retreat 20-30%.

2028: Chinese memory vendors may reach global tier-2 levels, potentially evolving the market from a three-horse race to four-way competition.

Get 3-5 key AI infrastructure signals weekly →

💬 Comments (0)